Some Ideas on Kam Financial & Realty, Inc. You Need To Know

Some Ideas on Kam Financial & Realty, Inc. You Need To Know

Blog Article

The smart Trick of Kam Financial & Realty, Inc. That Nobody is Discussing

Table of ContentsSee This Report on Kam Financial & Realty, Inc.The 7-Minute Rule for Kam Financial & Realty, Inc.Some Ideas on Kam Financial & Realty, Inc. You Should KnowWhat Does Kam Financial & Realty, Inc. Mean?The Best Strategy To Use For Kam Financial & Realty, Inc.Little Known Facts About Kam Financial & Realty, Inc..Rumored Buzz on Kam Financial & Realty, Inc.Unknown Facts About Kam Financial & Realty, Inc.

If your local region tax obligation price is 1%, you'll be billed a real estate tax of $1,400 per yearor a regular monthly residential or commercial property tax of $116. . We're on the last leg of PITI: insurance coverage. Look, everybody who gets a home needs home owner's insurance policyno ifs, ands, or buts concerning it. That's not always a poor thing.What an alleviation! Keep in mind that wonderful, elegant escrow account you had with your real estate tax? Well, guess what? It's back. Similar to your building tax obligations, you'll pay part of your homeowner's insurance costs on top of your principal and interest repayment. Your lending institution collects those repayments in an account, and at the end of the year, your insurance provider will attract all that cash when your insurance settlement is due.

Unknown Facts About Kam Financial & Realty, Inc.

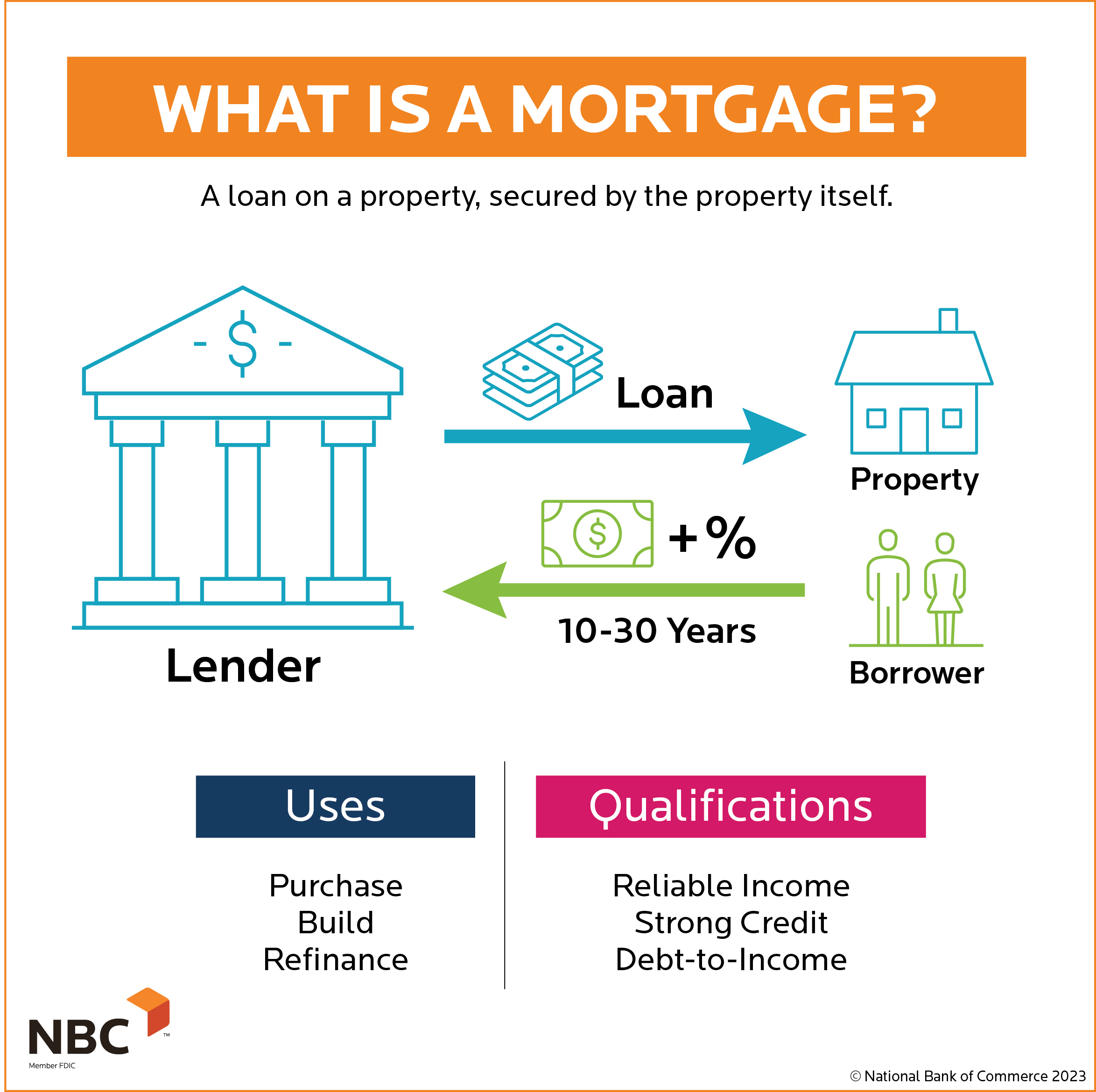

It's implied to secure the lending institution from youwell, a minimum of from the possibility that you can't, or just flat don't, make your mortgage payments. Naturally, that would never be youbut the lender doesn't care. If your down payment is less than 20% of the home's price, you're going to obtain penalized PMI.

If you come from an area like among these, don't neglect your HOA charge. Depending upon the age and size of your house and the facilities, this could add anywhere from $50$350 to the quantity you pay every month for your general real estate expenses. There are numerous sorts of mortgages and they all charge various month-to-month repayment amounts.

The Basic Principles Of Kam Financial & Realty, Inc.

Because you intend to obtain a mortgage the smart method, get in touch with our pals at Churchill Home mortgage - mortgage lenders in california. They'll stroll with you every action of the means to place you on the best path to homeownership

The Single Strategy To Use For Kam Financial & Realty, Inc.

This is one of the most typical sort of home mortgage. You can select a term as much as 30 years with most lenders. The majority of the very early payments pay off the interest, while the majority of the later repayments settle the principal (the initial quantity you obtained). You can take a table funding with a fixed price of rate of interest or a floating price. (https://www.sooperarticles.com/authors/786797/lupe-rector.html).

Most loan providers bill around $200 to $400. This is typically negotiable. california loan officer.: Table finances offer the technique of regular repayments and a collection day when they will certainly be paid off. They provide the assurance of recognizing what your payments will be, unless you have a floating rate, in which instance repayment quantities can transform

All about Kam Financial & Realty, Inc.

Revolving credit car loans work like a huge overdraft account. Your pay goes straight into the account and costs are paid of the account when they schedule. By keeping the finance as reduced as possible any time, you pay less interest due to the fact that lending institutions compute rate of interest daily. You can make lump-sum payments and redraw cash approximately your limitation.

Application charges on revolving credit rating home lendings can be approximately $500. There can be a charge for the day-to-day financial transactions you do via the account.: If you're well organised, you can repay your home loan much faster. This likewise suits people with uneven earnings as there are no fixed payments.

Kam Financial & Realty, Inc. for Beginners

Subtract the financial savings from the complete funding amount, and you just pay rate of interest on what's left. The even more cash you maintain across your accounts daily, the much more you'll save, because passion is computed daily. Connecting as several accounts as possible whether from a companion, parents, or various other family participants indicates even less passion to pay.

What Does Kam Financial & Realty, Inc. Do?

Settlements begin high, but minimize (in a straight line) with time. Costs are comparable to table loans.: We pay much less interest overall than with a table funding due to the fact that early repayments consist of a higher repayment of principal. These might match consumers who anticipate their earnings to drop, for instance, if one companion plans to offer up work in a couple of years' time.

We pay the interest-only part of our payments, not the principal, so the repayments are reduced. Some debtors take an interest-only financing for a year or 2 and after that switch to a table funding. The regular table lending application charges apply.: We have much more cash money for various other points, such as restorations.

Facts About Kam Financial & Realty, Inc. Revealed

We will certainly still owe the total that we obtained until the interest-only duration ends and we begin repaying the car loan.

The mortgage note is generally recorded in the public records along with the mortgage or the act of trust fund and serves as evidence of the lien on the property. The mortgage note and the home loan or action of trust are 2 different records, and they both serve look what i found various legal purposes.

Report this page